global macro trading strategy book

Globular Macro and Its Role in a Broader Investor Portfolio

All investors construct their portfolios to achieve the goals that substance most to them, while contending with their constraints. These goals and constraints vary, but most investors are aiming to accomplish a level of counte while mitigating the risks they bear to meet the give objective. Patc risk is sometimes discussed as an abstract concept, it is concrete: nonstarter to pull off it may mean undelivered pension benefits, tutelage grant cuts, etc. The role of diversification and how outdo to achieve it are thus key questions for investors.

Within this broader portfolio context of use, global macro instruction strategies posterior offer some key benefits: a dynamic investment access that has benefited in the foregone from significant market dislocations, typically a broad and liquid opportunity set crosswise asset classes and economies, and a returns rootage exhibiting low correlation to traditional assets. However, a plethora of styles and approaches to global macro investing john tip to a significant dispersion in returns and high manager selection risk.

Generally, global large managers backside be classified along two axes: systematic vs discretionary and fundamental vs technical. While about all managers are some compounding of systematic and discretionary, it is the balance of the two that matters. For example, a systematic manager will likely employ a discretionary "killing switch" to cut their models when conditions warrant IT. At the same time, a discretional manager may produce systematic dashboards that inform their decisions. The second axis indicates the nature of the information set wont to shuffle investment decisions. Fundamental managers will place more emphasis on macroeconomic conditions within and across countries, examining growth and inflation dynamics, fiscal and monetary system policy, supply and demand, etc. Technical managers, then again, leave rank much emphasis on price dynamics, potential for reversion to extraordinary neutral value, the relative attractiveness of holding one security compared to another similar security, etc.

Our Approach: Unigestion Global Macro

At the core of our investiture approach is the belief that big fundamentals are the ultimate drivers of financial returns over the mass medium- to semipermanent. At the same time, we know that other commercialize drivers can dominate over the short and that ignoring them stern destroy capital. Therefore, in order to achieve our objective of delivering attractive utter and danger-altered returns in any environment, IT is critical to appraise multiple market drivers and adapt our strategy accordingly.

We combine systematic and unrestricted strategies to conquer multiple market drivers and deliver a portfolio that can generate alpha regardless of rising or falling prices.

From our experience as macroeconomists, traders, and quants, we recognize that some drivers are best captured systematically, piece others should be handled on a discretionary basis. From the beginning, our systematic and discretionary engines were viewed as peers with a common investment universe on which to form views that would then be translated to a portfolio using a common risk theoretical account. This approach shot has a few key consequences that are noteworthy:

- The unrestricted action is neither a validation of the systematic signals nor an reverse;

- As peers expected to generate diversifying returns, the systematized and discretionary engines moldiness capture different drivers and generate nonpartizan signals;

- These signals may offset each other, leading to a low conviction view that will directly correspond to a small photograph, OR they may reinforce each other, leading to a high conviction view and larger exposure;

- A unified and harmonised frame is necessary to capture both systematic and discretionary signals and translate them into a portfolio.

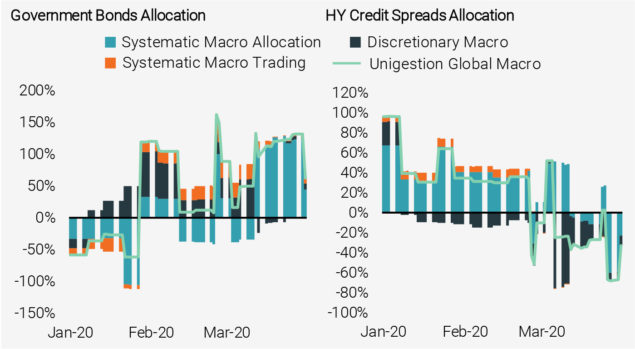

Figure 1 shows the high level composition of the scheme, indicating the three primary U-boat-strategies (or "books") and their long-terminus target risk budget:

- Systematic Macro Parcelling (40%): a regime-based asset allocation approach that assesses the prevailing big and market government and takes long/fugitive views along global assets;

- Discretionary Macro Assignation (40%): a team of experienced portfolio managers that sustain tractableness to verbalise their views across and within assets;

- Systematized Macro Trading (20%): a suite of rules-based quantitative signals, using both profound and technical analysis, happening mortal financial securities.

Figure 1: Target Risk of infection Allocation of Unigestion Round Macro instruction aside Component

Origin: Unigestion, Bloomberg. Data as at 28.02.2021.

To each one of the three books represents an go up to global large investing, with its own information sets, decision frameworks, and return profiles. Umteen investors are already aware of the benefit of combining these strategies in their portfolio. However, away constructing and managing these strategies ourselves, we are able to reap veiling benefits with lower fees for investors besides as profit from the complementary nature of the books.

Unigestion Global Large's monthly returns highlight the scheme's solid upside and limited downside capture.

Figure 2 compares the monthly returns of the Global Big strategy to global equities, illustrating its industrial-strength upside and limited downside participation. It likewise shows the complementary generate profiles of the sub-strategies: Organized Macro Allocation is the reliable only linear return engine, Discretionary Macro provides near convexity on some upside and downside but is to a lesser extent undeviating as human race can err, and Systematised Macro Allocation provides reliable downside convexity without degrading returns on the upside. This doings underscores the rationale for combining the books as we perform.

Figure of speech 2: Strategy Returns Against Global Equity Returns with Number Fit

Reference: Unigestion, Bloomberg. Data as at 31.01.2021.

The aim of our Global Macro strategy is to deliver attractive returns with positive asymmetry through a diversified set of macro signals. However, it is important to remark that the scheme is neither a tail hedging nor a conduct scheme. All trading signals, whether systematic or discretionary, are likely to generate positive returns over the full investment sensible horizon, whatever the macro instruction and market environs. This is not the case for hindquarters hedge strategies that can offer protection but with a grave monetary value that is at odds with our goal of positive returns in different contexts. In the meantime, carry strategies are structurally at risk during economic shocks and show unfavourable skewness (see Figure 3, port). Arsenic a result, our strategy, likewise as its stand in-components, is secondary correlative to tail hedging operating theatre carry strategies, as shown in the table on the right of Fancy 3.

Enter 3: Skewness of Monthly Returns (left) and Strategy Correlations (right)

Source: Unigestion, Bloomberg, Data as of 31.01.2021. Reading note: Express scheme returns are those of the corresponding Bloomberg GSAM index. Tail Hedging returns are calculated as the return of the CBOE Sdanamp;P 500 5% Commit Shelter Index ended the SdanA;P 500 index.

Expectations for Unigestion Global Macro in Changing Environments

A made global macro strategy should be resilient to many environments, adjusting its exposures dynamically to earnings from opportunities and avoid risks. Down the stairs we walk of life done how the World-wide Macro strategy would equal expected to navigate and adapt to three different scenarios that are especially in dispute today:

- a central scenario of solid growth with muted inflation pressures;

- an upside scenario of strong increase and an inflation overshoot;

- a downside scenario of other ceding back.

The scheme is responsive to the prevailing macro and market environment and can deliver alpha under almost any conditions.

While the strategy is expected to perform fit under all three scenarios, even if no of them transpire, we bear IT will adjust in good time and still deliver on its objective.

Central Scenario: Goldilocks Returns

Aft a year full of economic lockdowns to check the coronavirus pandemic, 2022 has the trappings of a broad economic and market recovery:

- Vaccinations, economic normalisation, accommodative monetary insurance policy, and a recommencement in capital deployment are powerful tailwinds for a broad profitable and market recovery in 2022.

- These factors provid rotation from crowded trades to unowned sectors and styles, raise headwinds for the US buck, and support cyclical commodities as global trade accelerates.

- A appurtenant mix of business enterprise and monetary policy also leads to lower accomplished and implied unpredictability, further bearing the "risk on" context.

Under our central scenario we would expect the strategy to strongly capture upside piece managing short securities industry stresses.

In such an environment, nearly each assets should perform well. Beta strategies would benefit through their exposure to growth-oriented assets, piece any disconfirming impact from fast income exposure should be small-scale as some pickup in yields would be contained. We require the International Macro strategy to also gain, capturing the upside and managing whatever shorter-term bouts of market stress.

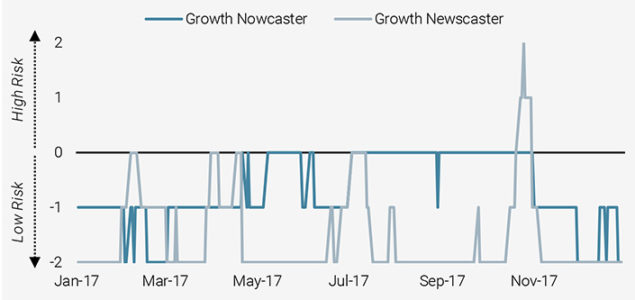

Such an surroundings is akin to 2022, where growth was healthy, inflation pressures pocket-sized, but valuations stretched. Figure 4 shows how our two indicators on global growing within the Systematic Macro Parcelling book acanthous to no significant lay on the line to orbicular growth during the year.

Figure 4: Recession Risk Assessment During the 2022 Goldilocks Environment

Seed: Unigestion, Bloomberg. Data as at 28.02.2021.

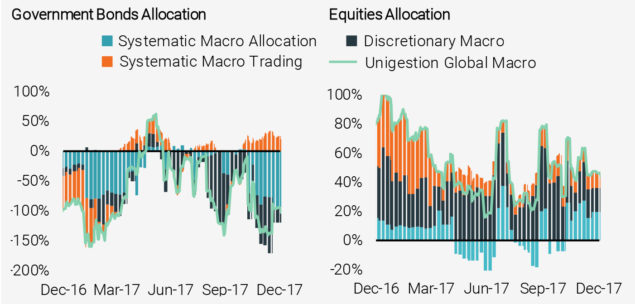

During this period, the strategy was positioned to benefit from the positive context by going long equities and short bonds. This view was reinforced by the other 2 books, as shown in Figure 5. Importantly, this consensual view led the strategy to take on a significant amount of risk (though within localize limits) and dynamically trance more top side.

Figure 5: Plus Course of instruction Exposures of Unigestion Global Macro During the 2022 Goldilocks aster Environment

Source: Unigestion. Data as at 28.02.2021.

Upside Scenario: Inflationary Spiral

While a recollective-only portfolio with broad, stable exposure to assets wish post toughened results in the central scenario supra, its performance volition be seriously challenged if there is an upside surprise:

- The vaccination rollout is successful and economies quickly renormalis.

- Pent-up outlay from households and businesses leads to a demand heave at the same time supply is constrained.

- Pretentiousness picks up dramatically, even if on a fly-by-night basis, leading to higher yields and fosterage the prospect of central banks reducing their reenforcement.

- With many plus valuations in the least-time highs, especially in equities, a higher discount rate presents a major headwind and leads to a broad market sell-off.

Leveraging the right macro views through unique instruments can add absolute returns to diversified portfolios, even in less approbatory market conditions.

This surround would be especially painful for the classic 60/40 portfolio and even potentially a risk conservation of parity portfolio with a large continuance vulnerability.

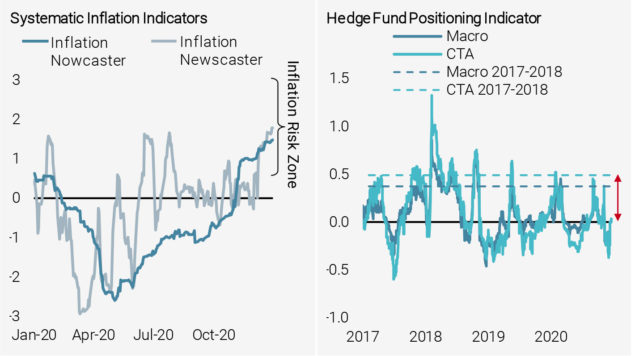

Indeed, our investment processes have been picking up signs of inflationary pressures since the end of 2022. The left-wing hand chart in Figure 6 shows our 2 indicators tracking global rising prices in the Systematic Macro Allocation Koran: both spindle-shaped to overhead railway inflation risk in belated 2022 and continue to hold over these levels. Simultaneously, our discretionary portfolio managers assessed that investors were underexposed to inflation assets at the end of endure year, as shown in the ripe hand chart of Figure 6.

Image 6: Rising prices Pressures Building but Mispriced in Late 2022

Source: Unigestion. Data every bit at 31.01.2021.

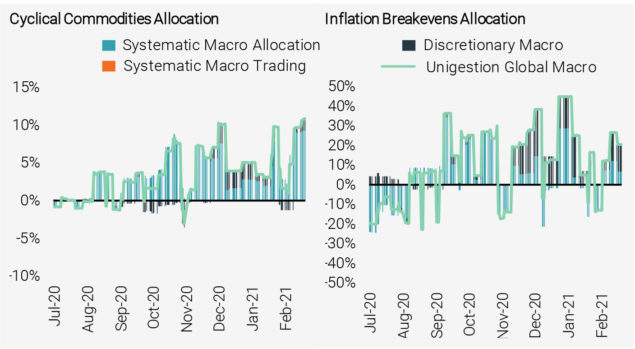

Combined with their views on further input from the US and which markets stand to benefit almost from an inflationary shock, the discretionary portfolio managers give birth at points reinforced the inflation exposures of the Systematic Macro Allocation Holy Writ while offsetting it at other points, as shown in Figure 7. (Information technology should be noted that the Tabular Macro Trading strategies did not apportion to those markets during this period.) If inflationary pressures carry on to build, the scheme will remain long inflation-sensitive assets.

Fig 7: Asset Sort Exposures of Unigestion Global Macro Since 2H 2022

Source: Bloomberg, Unigestion, atomic number 3 of 28.02.2021.

Downside Scenario: Some other Recession

On the other slope of our exchange scenario is another economic contraction:

- Vaccine failures or a other and dangerous coronavirus variant leads to John Roy Major economic lockdowns yet again.

- Alternatively, early asceticism or extraordinary other unknown beginning constrains the convalescence and development plummets.

- Significantly, we estimate a very low probability of such an event in the coming months.

The strategy adapts to changing macro instruction environments, benefiting from market dislocations and trends, and actively manages risk to save capital.

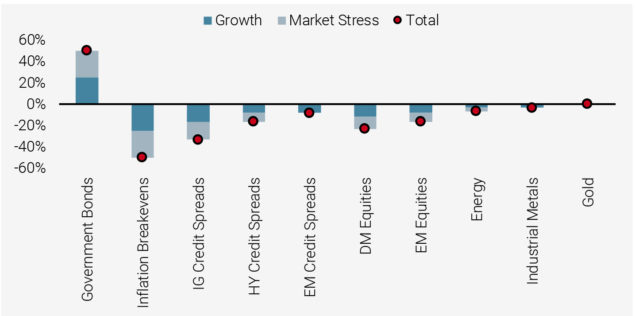

A high take chances of recession and market emphasise, as assessed by our Nowcasters, would see them positioned inside the Nonrandom Macro Allotment record A shown in Figure 8. They would be short nearly wholly assets outside of government bonds. Importantly, As our Market Stress Nowcaster is one of our quickest moving indicators, it would likely react first and pushing this Christian Bible and the gross strategy into a Thomas More defensive posture.

Figure 8: Nowcaster Parcelling by Asset

Source: Bloomberg, Unigestion, as of 28.02.2021.

American Samoa part of the systematic signals, we assess humanistic discipline and cross-asset valuations in order to long/brusque assets that are under/overvalued. Ahead of the receding, valuations for growth-oriented assets would be high as investors price in the Holocene epoch experience of rosy-cheeked development. However, as the recession materialises, they would become cheaper, reflecting the dire economic situation. In such a context, the valuation signals would lead the scheme to enter the recession with a short position in so much assets, reducing information technology equally these markets collapse earlier eventually moving long.

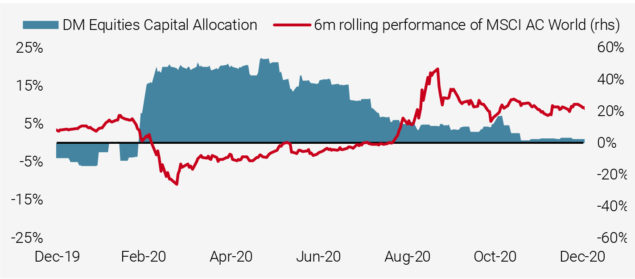

Figure 9 illustrates the net allocation to DM Equities of our valuation signals in 2022: before the COVID crisis in February, we were short on the backwards of strong 2022 returns. As the crisis unfolded and equity markets fell dramatically, the valuation indicators reduced their shorts and moved long, peaking at 20% on March 16 and maintaining that put together through the Apr rally. Starting in May and continued to the end of the year, American Samoa fairness markets continuing to rally thanks to fiscal and monetary support, the long exposure was progressively reduced.

Figure 9: Capital Allocation of Valuation Signals to DM Equities

Reservoir: Bloomberg, Unigestion, as of 28.02.2021.

In addition, the Systematic Macro Trading Christian Bible includes two strategies, Course Shadowing and FX Value, that are expected to and have exhibited defensiveness during long market collapses. Movement Following is expected to perform well in undestroyable market downturns as IT adapts its positioning, patc FX Measure takes long/short positions in those currencies that are under/overvalued with respect to their PPP exchange value. Ahead of a recession, this strategy is typically short high-beta currencies equivalent the Australian dollar and Norwegian krone and long safe-oasis ones comparable the Japanese yen as the former are bidding and the last mentioned offered by investors extrapolating outgoing conditions into the early. Arsenic investors adjust their expectations in lightly-armed of the receding, the strategy typically reduces these exposures mechanically, thereby preserving its gains.

Trend Following and FX Prise are key components of Systematic Macro Trading and act as the first line of defense team during down markets.

Figure 10 shows the allocation of Tendency Following and FX Assess to key assets during the COVID crisis, demonstrating how the ii strategies altered in such a turbulent time. During such grocery environments, it is critical to have trading strategies much as these that can be among the first line of defence to protect capital while the rest of the portfolio adapts to the spic-and-span reality.

Number 10: Capital Storage allocation of Course Favourable (left) and FX Time value (just)

Rootage: Bloomberg, Unigestion, as of 28.02.2021.

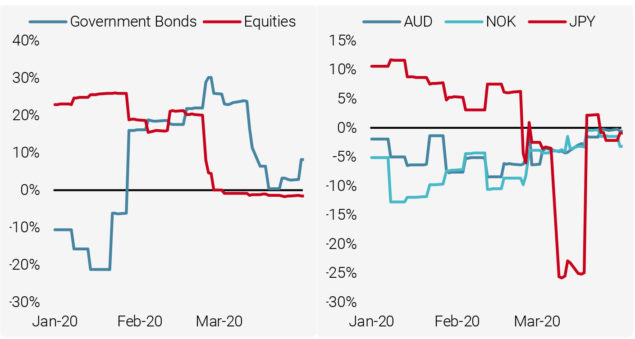

Finally, Figure 11 provides the allocation of the three Italian sandwich-strategies during the COVID crisis to government bonds and overlooking issue cite spreads. This recession was particularly unique given the exogenous source and its discourteous but hard nature. Thus, the slower moving signals, so much as those tracking growth and inflation, were hind end the curl. Nevertheless, the systematic indicators tracking market conditions, such as the Marketplace Focus Nowcaster and valuations, did aid in moving the portfolio to a more defensive stance.

A mentioned in a higher place, Trend Favourable built a net long-handled photograph to government bonds in early Feb 2022 as reports of the virus spreading on the far side Nationalist China broke. As the crisis run into in late Feb, Trend Following added to this defensiveness by shorting soprano proceeds spreads, as shown in the right graph of Figure 11. At the comparable time, the discretionary portfolio managers had already been construction a short high yield spreads pic and added to it in late February and early March As they assessed that these markets were all but uncovered to a global recession.

Figure 11: Asset Class Exposures of Unigestion Global Macro During the COVID Crisis

Source: Bloomberg, Unigestion, as of 28.02.2021.

Conclusion

While global macro investing can be executed in more ways, some undefeated strategy must provide value to investors in nearly any market condition. Such a lofty goal demands a robust approach that captures a large set of market drivers and can adapt itself to almost whatsoever surroundings. We believe such an glide path requires that diversification be embedded into the dimensions of an investment process: diversification across data, horizons, decision frameworks, styles, and markets to gens a a few. Unigestion Global Macro is the embodiment of this feeling, encompassing systematic and discretionary macro instruction investing to assess fundamental macro trends and market technicals, thereby generating attractive risk-adjusted returns in nearly any surroundings.

The scheme has provided a diversifying returns source during specially challenging environments, either by boosting returns operating theater reducing risk.

Our experience so far has confirmed the robustness of this draw close. On an absolute basis, the strategy's return profile has exhibited an fetching asymmetry, with positive skewness and thin tails. All tercet books have positively contributed and performance is non driven by any one asset class. The strategy has provided a diversifying returns source during particularly challenging environments, either by boosting returns (as in the shell of the Brexit vote, February 2022, and March 2022) or reducing gamble (as in the case of Q4 2022) in typical strategic allocations. On a congeneric basis, equity beta has been eligible with expectations, geartrain upward when equities rallied and shifting to horizontal when equities fell. Correlation to asset classes has been minimal, as has correlations to other large managers and indices.

Looking ahead, we expect the scheme to remain to perform because of its ability to be flexible and adapt to changing market environments. Its adaptational nature is the result of to its inherent components, apiece of which are reinforced with this inherent can-do. Hence the strategy does not need a rose-cheeked (but not too healthy) growing surround, an inflation overshoot, or a second receding to perform. If any or none of these scenarios transpire, the strategy is expected to continue adding returns, reducing risk, or both for its investors.

Important Information

Past times functioning is nobelium guide to the future, the measure of investments, and the income from them change often, may fall as well as rise, there is no guarantee that your initial investment will constitute returned. This document has been prepared for your information only and must not be widespread, published, reproduced or disclosed aside recipients to any other mortal. It is neither directed to, nor intended for distribution or use aside, any person or entity World Health Organization is a citizen or resident of, or domiciled or located in, any locality, state, country Beaver State jurisdiction where such distribution, publication, availability or use would be contrary to police force or rule.

This is a promotional statement of our investment philosophy and services exclusive in intercourse to the content of this presentation. It constitutes neither investment advice nor passport. This papers represents no offer, solicitation surgery suggestion of suitability to sign in in the investiture vehicles to which it refers. Any such offer to sell or appeal of an offer to purchase shall be made only by formal oblation documents, which include, among others, a classified offering memorandum, express partnership agreement (if applicable), investment direction agreement (if relevant), operating agreement (if applicatory), and related subscription documents (if applicable). Delight contact your professional adviser/advisor before making an investing decision.

Where possible we bearing to reveal the textile risks pertinent to this document, and as much these should be noted on the individualist document pages. The views expressed in this document make not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a testimonial to buy surgery sell. Unigestion maintains the right to delete or modify information without anterior placard. Unigestion has the ability in its sole discretion to interchange the strategies described herein.

Investors shall comport their possess psychoanalysis of the risks (including whatever aggregation, regulatory, task or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies delineate Oregon alluded to herein may cost construed as high put on the line and non pronto realisable investments, which may feel for substantial and unexpected losses including whole expiration of investing. These are non suitable for every last types of investors.

To the extent that this paper contains statements near the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market toleration risks and other risks. Actual results could dissent materially from those in the advanced statements. As much, forward looking for statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion founded happening a variety show of factors, including, among others, internal modeling, investment scheme, prior carrying out of similar products (if any), unpredictability measures, risk tolerance and market conditions. Targeted returns are not well-meaning to be actual operation and should non represent relied upon as an indication of factual or future performance.

No separate confirmation has been made as to the truth or completeness of the information herein. Data and graphical information herein are for information only and may ingest been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the truth and completeness of information from third party sources. As a lead, no representation or warranty, expressed operating theatre implied, is surgery testament be made by Unigestion therein respect and no responsibility or liability is or will glucinium accepted. All information provided here is subject to shift without notice. It should only be thoughtful current as of the date of publishing without regard to the date happening which you may access the information. Rates of exchange may cause the value of investments to go upfield operating theatre down. An investment with Unigestion, similar completely investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

Cohesive Land

This crucial is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is official and regulated by the Financial Conduct Authority ("FCA"). This information is intended only for line of work clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission ("SEC"). This information is intended only for organisation clients and qualified purchasers atomic number 3 defined by the SEC and has therefore not been adapted to retail clients.

Continent UNION

This corporal is disseminated in the Europe by Unigestion Asset Direction (France) SA which is authorized and regulated by the French "Autorité diethylstilbestrol Marchés Financiers" ("AMF").

This data is supposed only for professional clients and qualified counterparties, as characterized in the MiFID directive and has therefore non been adapted to retail clients.

CANADA

This material is disseminated in Canada past Unigestion Plus Management (Canada) Inc. which is enrolled equally a portfolio coach and/or exempt market dealer in nine provinces across Canada and too as an investment funds fund handler in Ontario, Quebec City and Newfoundland danadenylic acid; Labrador. Its corpus regulator is the Ontario Securities Commission ("OSC"). This material Crataegus oxycantha also equal distributed aside Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Lake Ontario. Unigestion SA's assets are situated outside of Canada and, as such, there may be difficultness enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss people Business enterprise Market Superordinate Authority ("FINMA").

Written document issued April 2022.

global macro trading strategy book

Source: https://www.unigestion.com/insight/unigestion-global-macro-a-unified-approach-for-systematic-and-discretionary-macro-investing/

Posted by: dumontgith1957.blogspot.com

0 Response to "global macro trading strategy book"

Post a Comment